Updated 5/19/26

Why Many Teachers Also Build Wealth Outside of Their Pension

Missouri teacher pensions through PSRS can provide valuable lifetime income in retirement. However, one important thing many teachers do not realize is that pension benefits are generally designed for the retiree’s lifetime, not necessarily as a long-term inheritance asset for children.

**The general rule of thumb is if you want to leave more for your kids, your monthly benefit from PSRS is reduced.** So if you chose this, you can’t rely on full monthly benefits to support your life.

That is one reason many teachers also choose to build wealth in accounts they personally own, such as a Roth IRA.

Why a Roth IRA Can Be So Valuable for Teachers

A Roth IRA can complement a teacher pension in several important ways:

- tax-free growth

- tax-free retirement withdrawals if rules are met

- flexible investment options

- potential long-term benefits for spouses and children

While a pension is designed primarily to create retirement income during your lifetime, a Roth IRA can also become part of a family wealth plan.

Missouri teachers often ask how pension benefits compare to personally owned retirement accounts like Roth IRAs.

| Feature | PSRS Pension | Roth IRA |

|---|---|---|

| Lifetime Income | Yes | No |

| Tax-Free Growth | No | Yes |

| Flexible Investments | No | Yes |

| Can Pass to Kids | Limited | Yes |

| Can Pass to Spouse | Limited | Yes |

For many teachers, the pension provides retirement stability while the Roth IRA provides flexibility and potential family legacy benefits.

Roth IRAs Can Potentially Be Passed to a Spouse or Children

One advantage of a Roth IRA is that the account can usually transfer to beneficiaries after death.

For a Spouse

In many cases, a surviving spouse can continue treating the Roth IRA as their own retirement account. This can allow the money to continue growing tax-free for many additional years.

For Children

Children who inherit a Roth IRA may also receive important tax advantages compared to inheriting many traditional retirement accounts.

Although inherited Roth IRA rules have changed in recent years, these accounts can still provide:

- tax-free withdrawals if requirements are met

- continued tax-advantaged growth over time

- more flexibility than many pension structures

A Pension Provides Income. A Roth IRA Can Help Build Family Wealth

For many Missouri teachers, the pension becomes the foundation of retirement income.

But accounts like Roth IRAs may help provide:

- additional retirement flexibility

- tax diversification

- emergency access options

- assets that can potentially benefit FUTURE GENERATIONS

That is one reason many teachers choose to build both:

- guaranteed higher pension income

- personally owned investment accounts

Many teachers spend decades serving students and communities. Building wealth outside of the pension system can help create additional flexibility during retirement while also potentially providing financial benefits for a surviving spouse or future generations.

Generational Wealth Development. Build for the future. Change your kids’ lives.

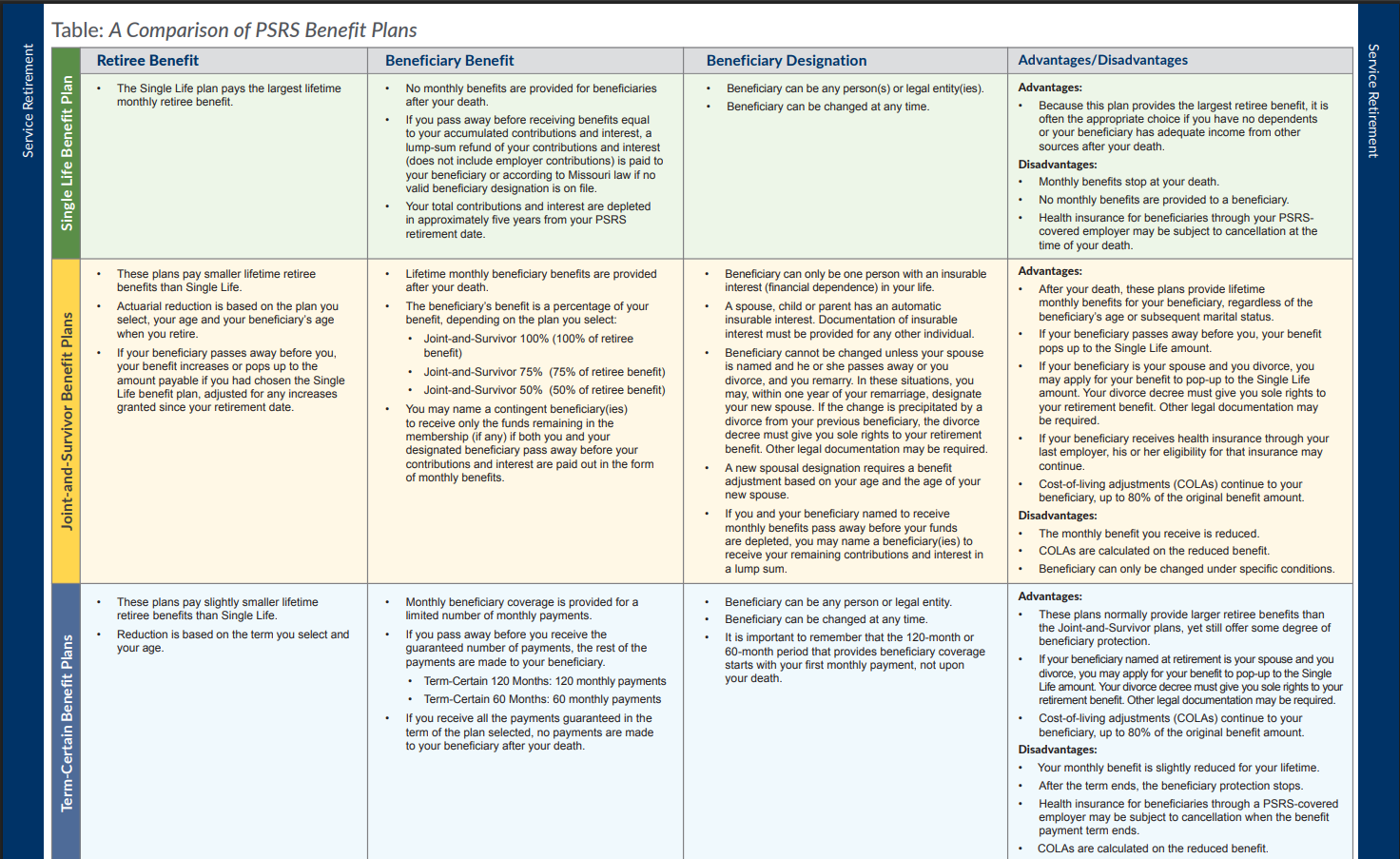

Here is the guide from PSRS 2025 Handbook

What You Should Know About Retirement When You Leave The Classroom

Leaving teaching is a big decision. You’ve poured your time, energy, and heart into helping students — and now you’re stepping into something new. Whether you’re changing careers, moving, or just ready for a different chapter, one of the biggest questions that comes up is: What happens to my Missouri Teacher Retirement?

If you’ve been teaching in Missouri, you’ve been paying into PSRS (Public School Retirement System) or PEERS (Public Education Employee Retirement System). What you do with that money when you leave really matters.

As a financial advisor in Missouri who works with teachers and young professionals, I talk with a lot of educators about this exact situation. Here’s what you should know before making any big moves.

Know Which Missouri Teacher Retirement System You’re In

If you’re a certified teacher, you’re in PSRS.

If you’re a school employee who isn’t certified — like a para, bus driver, or secretary — you’re in PEERS.

Both systems are designed to provide lifetime income after a full career in education. But if you leave before retirement age, you have some important choices to make about what happens next. You can access both systems here.

Option 1: Leave Your Money in PSRS or PEERS

If you’re vested, meaning you’ve worked enough years to qualify for a future pension, you can leave your money in the system. You won’t keep earning new service credit, but your benefit will still be there waiting when you reach retirement age.

This can be a smart move if you might come back to public education or if your PSRS or PEERS benefit is strong compared to what you’d earn investing on your own.

Option 2: Take a Refund of Your Contributions

You can request a refund, but this is where a lot of people get surprised. If you take your contributions as a direct payout, that money is considered taxable income. And if you’re under 59½, there’s usually a 10% early withdrawal penalty on top of that.

On top of taxes and penalties, you lose your pension benefit. Once you take your money out, you can’t put it back later if you return to teaching. That’s a decision that can’t be undone — so make sure you understand what you’re giving up.

Option 3: Roll It Over to an IRA or Another Retirement Plan

Another choice is to roll over your PSRS or PEERS balance into an IRA (Individual Retirement Account) or another qualified plan if your new employer allows it.

This option lets your money keep growing tax-deferred while giving you more control over your investments.

If you take this route, make sure you do a direct rollover, where the money moves straight from PSRS or PEERS to the new account. That way, you avoid taxes and penalties.

Some people also consider converting to a Roth IRA, which means paying taxes now in exchange for tax-free growth later. That can make sense in some situations — especially if you expect your income to go up in the future — but it’s important to plan ahead for the tax bill.

If you need to open an account to roll this into, that’s exactly what I can help you with. Reach me here.

A Quick Word About Taxes

Here’s the short version:

- Taking a refund → you’ll pay income tax (and possibly a penalty).

- Rolling over → no taxes now, as long as it’s a direct rollover.

- Converting to Roth → taxes now, but tax-free withdrawals later.

For more details, check out the official PSRS/PEERS Rollover Options Guide. It’s a helpful summary of how these options work and what the IRS rules say.

Before You Make a Decision

Before you decide what to do about your Missouri Teacher Retirement, take a few steps to make sure you’re on solid ground:

- Log in to your PSRS/PEERS account and see if you’re vested.

- Request a benefit estimate so you know what your pension would pay at retirement.

- Talk with a financial advisor who understands Missouri’s teacher retirement system and can help you see how each option fits into your bigger plan.

A little clarity now can save you a lot of taxes and headaches later.

Let’s Make a Plan Together for Your Missouri Teacher Retirement

If you’re a Missouri teacher thinking about leaving the classroom, I’d love to help you walk through your retirement options. We’ll look at your PSRS or PEERS benefits, what a rollover might mean for you, and how to make confident financial choices for your next chapter.

Schedule a quick chat with me — no sales pitch, just honest, practical advice from a Missouri financial advisor who helps teachers and young professionals build strong financial plans.

Disclaimer

Disclaimer: I do not, have not, and never will claim to be a professional writer. Please excuse any spelling and/or grammatical errors. All information provided is for educational purposes only and is not intended to be investment advice. The information being provided via hyperlinks may be from third-party websites and is strictly as a courtesy/convenience. When you link to any of the web sites provided here, you are leaving this website. I make no representation as to the completeness or accuracy of information provided on these websites. I am not a CPA or attorney and anything included in this article may not be interpreted as tax or legal advice.